为什么中国对欧洲的出口如此强劲? Why are China's exports to Europe so strong?

自2021年以来,中国对欧元区的出口大幅增长,出口量在2021年至2024年间增长了约75%。这种增长在汽车和钢铁等行业尤为明显。与此同时,中国的出口价格下降,使中国商品在欧洲市场更具竞争力。 China's exports to the euro area have grown significantly since 2021, with export volumes rising by around 75% between 2021 and 2024. This growth has been particularly pronounced in sectors such as motor vehicles and steel. At the same time, China's export prices have declined, making Chinese goods more competitive in European markets.

本文分析了中国对欧洲出口强劲表现背后的因素。文章认为,中国国内需求疲软,而非从美国转移的贸易,是中国对欧洲出口增长的主要驱动力。 This box examines the factors behind China's strong export performance to Europe. It argues that weak domestic demand in China, rather than trade diversion from the United States, is the primary driver of China's export growth to Europe.

主要发现 Key findings

- 自2021年以来,中国的出口价格大幅下降,而出口量大幅增加。 China's export prices have declined significantly since 2021, while export volumes have increased substantially.

- 2021年房地产危机后,中国国内需求疲软,导致企业将销售转向海外市场。 Weak domestic demand in China, following the 2021 real estate crisis, has led firms to redirect sales toward foreign markets.

- "剩余出口"理论有助于解释近期的贸易模式:国内销售表现不佳的企业比国内销售强劲的企业增加了更多出口。 The "vent-for-surplus" theory helps explain recent trade patterns: firms with underperforming domestic sales have increased exports more than those with strong domestic sales.

- 在解释中国对欧洲出口增长方面,从美国到欧洲的贸易转移不如国内需求疲软重要。 Trade diversion from the United States to Europe is less important than weak domestic demand in explaining China's export growth to Europe.

中国的出口价格和竞争力 China's export prices and competitiveness

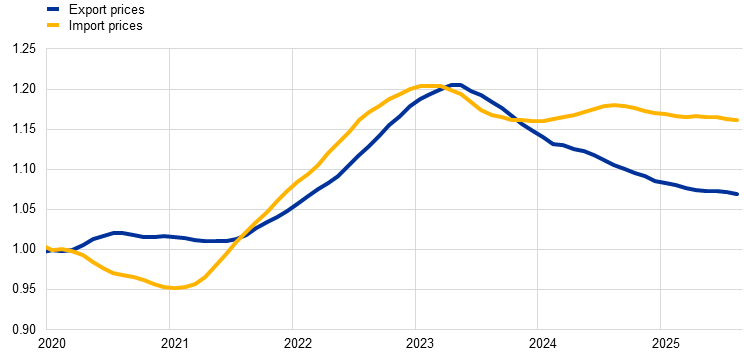

自2021年以来,中国的出口价格大幅下降(图表D)。与此同时,持续的产业升级、技术进步和产品质量的提高增强了非价格竞争力。既定的贸易关系和中国融入全球价值链进一步巩固了其市场地位,使其能够在海外扩大市场份额(Al-Haschimi等人,2024b)。 China's export prices have declined significantly since 2021 (Chart D). At the same time, ongoing industrial upgrades, technological advancements and improvements in product quality have enhanced non-price competitiveness. Established trade relationships and China's integration into global value chains have further strengthened its market position and enabled it to expand market shares abroad (Al-Haschimi et al., 2024b).

国内需求疲软,加上出口价格疲软,最近在中国出口动态中发挥了核心作用。2021年的国内房地产危机严重抑制了家庭需求。与此同时,旨在在中国供给侧导向的财政方法下稳定增长的国家主导的制造业投资,对消费的直接支持很少。产能过剩导致企业陷入价格战。这侵蚀了利润率,在劳动力过剩的通缩环境中抑制了支出——促使企业将销售转向海外市场。[3] 这种转变反映了国际贸易的"剩余出口"理论,该理论认为,需求驱动的国内销售下降会产生可以转向海外的过剩产能。[4] 该机制假设短期内的固定投资,这在中国尤其相关,因为投资往往由中央计划指导。为了在海外扩张,企业必须在外国市场获得竞争力。它们通常通过降低短期边际成本和价格,或接受更窄的利润率,在某些情况下甚至接受亏损来实现这一目标。 Subdued domestic demand, along with weak export prices, has recently played a central role in China's export dynamics. The 2021 domestic real estate crisis sharply curtailed household demand. At the same time state-led manufacturing investment, aimed at stabilising growth under China's supply side-oriented fiscal approach, offered little direct support to consumption. Excess capacity has led firms into price wars. This has eroded profit margins and discouraged spending in a deflationary environment with significant labour slack – prompting firms to redirect sales toward foreign markets.[3] This shift reflects the "vent-for-surplus" theory of international trade, which posits that a demand-driven decline in domestic sales generates excess capacity that can be redirected abroad.[4] The mechanism assumes fixed investment in the short term, which is particularly relevant in China, where investment is often guided by central planning. To expand abroad, firms must gain competitiveness in foreign markets. They typically do so by reducing short-run marginal costs and prices, or by accepting narrower profit margins, and in some cases even losses.

"剩余出口"理论有助于解释近期的贸易模式 The "vent-for-surplus" theory helps explain recent trade patterns

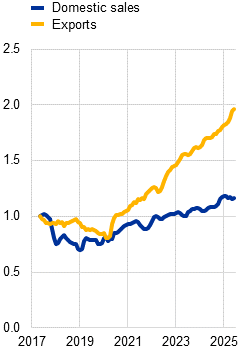

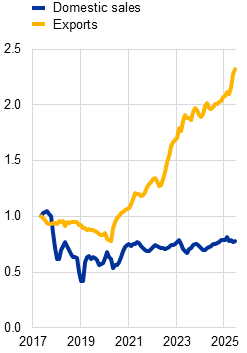

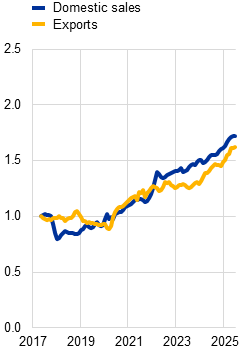

实际国内销售的代理指标表明,自疫情以来,实际出口超过了国内销售,导致两者之间的差距扩大(图表E,面板a)。我们的分析发现,在国内销售增长表现不佳的行业中,出口增长最为强劲。自2022年以来,汽车和钢铁等行业的出口量增长了约75%(图表E,面板b),这表明企业越来越多地将销售转向海外市场。通过降低价格来吸收国内过剩产能受到需求疲软的制约,因为住房低迷继续拖累消费者信心。相比之下,在国内销售增长表现优异的行业,主要与科技产品相关,出口量大致与国内销售同步,自2022年以来增长了约30%(图表E,面板c)。所有行业的出口价格都有所下降,出口增长较强的行业下降更为明显。 Proxies for real domestic sales indicate that, since the pandemic, real exports have outpaced domestic sales, resulting in a widening gap between the two (Chart E, panel a). Our analysis finds that export growth is strongest in sectors with underperforming domestic sales growth. Since 2022 export volumes in sectors such as motor vehicles and steel have risen by about 75% (Chart E, panel b), suggesting that firms have increasingly shifted sales to foreign markets. Domestic absorption of excess capacity through lower prices has been constrained by weak demand, as the housing downturn continues to weigh on consumer confidence. By contrast, in sectors with outperforming domestic sales growth, mainly related to technology goods, export volumes have largely moved in line with domestic sales, rising by about 30% since 2022 (Chart E, panel c). Export prices have declined across all sectors, with more pronounced declines in sectors recording stronger export growth.

国内需求疲软似乎是缺失环节 Weak domestic demand appears to be the missing link

国内需求疲软似乎是解释中国对欧洲出口强劲的缺失环节——比与关税相关的贸易转移更重要。中美之间不断升级的贸易紧张局势可能导致中国对欧洲的出口进一步转移。然而,中国对欧盟出口的增长早于最新的紧张局势,而是与中国国内需求疲软的开始同时发生。2024年第四季度,国内销售的平均月价值约为总出口的四倍,是对美国出口的28倍以上。这表明可以转移到欧盟的商品池比仅贸易数据所显示的要广泛得多。即使将国内销售的一小部分转移到海外,也可能比从美国转移大量出口更能推动整体出口——包括对欧盟的出口。[5] Weak domestic demand appears to be the missing link in explaining China's strong exports to Europe – more so than tariff-related trade diversion. Escalating trade tensions between the United States and China might result in a further diversion of Chinese exports to Europe. However, the rise in China's exports to the EU predates the latest tensions and coincides instead with the onset of weakness in domestic demand in China. In the fourth quarter of 2024 the average monthly value of domestic sales was around four times higher than total exports and over 28 times larger than exports to the United States. This suggests the pool of goods that could be redirected to the EU is much broader than trade data alone would suggest. Redirecting even a small share of domestic sales abroad could boost overall exports – including to the EU – more than a sizeable diversion of exports from the United States.[5]

参考文献 References

参考文献: Reference: Al-Haschimi, A. 和 Spital, T. (2024a),"中国增长模式的演变:挑战和长期增长前景",《经济公报》,第5期,ECB。 Al-Haschimi, A. and Spital, T. (2024a), "The evolution of China's growth model: challenges and long-term growth prospects", Economic Bulletin, Issue 5, ECB.

参考文献: Reference: Al-Haschimi, A., Emter, L., Gunnella, V., Ordoñez Martínez, I., Schuler, T. 和 Spital, T. (2024b),"为什么与中国的竞争比以往任何时候都更加激烈",《ECB博客》,ECB,9月3日。 Al-Haschimi, A., Emter, L., Gunnella, V., Ordoñez Martínez, I., Schuler, T. and Spital, T. (2024b), "Why competition with China is getting tougher than ever", The ECB Blog, ECB, 3 September.

参考文献: Reference: Almunia, M., Antràs, P., López-Rodríguez, D. 和 Morales, E. (2021),"释放:国内衰退期间的出口",《美国经济评论》,第111卷,第11期,第3611-62页。 Almunia, M., Antràs, P., López-Rodríguez, D. and Morales, E. (2021), "Venting Out: Exports during a Domestic Slump", American Economic Review, Vol. 111, No 11, pp. 3611-62.

参考文献: Reference: Boeckelmann, L., Emter, L., Gunnella, V., Klieber, K. 和 Spital, T. (2025),"中美贸易紧张局势可能给欧洲带来更多中国出口和更低价格",《ECB博客》,ECB,7月30日。 Boeckelmann, L., Emter, L., Gunnella, V., Klieber, K. and Spital, T. (2025), "China-US trade tensions could bring more Chinese exports and lower prices to Europe", The ECB Blog, ECB, 30 July.

参考文献: Reference: Chen, T., Hsieh, C.-T. 和 Song, Z.M. (2022),"美中贸易战中的非关税壁垒",《NBER工作论文系列》,第30318号,美国国家经济研究局。 Chen, T., Hsieh, C.-T. and Song, Z.M. (2022), "Non-Tariff Barriers in the U.S.-China Trade War", NBER Working Paper Series, No 30318, National Bureau of Economic Research, Inc.

脚注 Footnotes

脚注 1: Footnote 1: "中国制造2025",于2015年启动,是中国将制造业从劳动密集型升级为高科技产业的战略。该计划旨在通过提高国内含量和促进创新以及高附加值行业(如电动汽车、半导体、航空航天、机器人和生物技术)来实现更大的自给自足。 "Made in China 2025", launched in 2015, is China's strategy of upgrading its manufacturing sector from labour-intensive to high-tech industries. The plan aims to achieve greater self-reliance by boosting domestic content and promoting innovation and higher value-added sectors, such as electric vehicles, semiconductors, aerospace, robotics and biotechnology.

脚注 2: Footnote 2: 关于中国低出口价格和非价格竞争力的讨论,见Al-Haschimi等人(2024b)。 For a discussion of China's low export prices and non-price competitiveness, see Al-Haschimi et al. (2024b).

脚注 3: Footnote 3: 关于疫情后的出口动态,见Al-Haschimi和Spital(2024a)。 On export dynamics following the pandemic, see Al-Haschimi and Spital (2024a).

脚注 4: Footnote 4: 见Almunia等人(2021)。 See Almunia et al. (2021).

脚注 5: Footnote 5: 关于中国出口向欧元区转移的讨论,见Boeckelmann等人(2025)。 For discussion on the redirection of Chinese exports to the euro area, see Boeckelmann et al. (2025).